This is a level (3+ to 4+) mathematics in science contexts activity from the Figure It Out series.

A PDF of the student activity is included.

Click on the image to enlarge it. Click again to close. Download PDF (962 KB)

Students will:

- practise inductive reasoning

- calculate percentages and rates for savings and loans.

Students should discover that:

- small changes over time can lead to big savings.

a calculator (optional)

Preparation and points to note

Like a number of other activities in this book, Saving Power takes students into unfamiliar territory and asks them to engage with adult scenarios – in this case, a scenario that involves power bills, loans, and savings. To get to the mathematics, they have to read and interpret the scenario and the questions.

All students bring with them a variety of experiences that will or will not have given them confi dence that they can solve problems embedded in words. Problem solving can’t be taught by always dissecting the information for students and rescuing them the moment they put their hand up. Students need to be given the tools, see their use modelled, and then learn how to choose and fl exibly apply an increasing kit of tools to new problems. They need to learn that getting stuck is part of every problem-solving experience. (If they don’t get stuck, the “problem” is not a problem!) They also need to learn that they must grapple with the diffi culties until they fi nd a way forward. Every time they do this and succeed, they strengthen their identities as learners of mathematics (“I can solve problems.”)

The critical thinking needed for evaluating results is a suitable key competency focus for these activities.

Points of Entry: Mathematics

Several questions in this activity require inductive reasoning or leaps in thinking. Encourage the students to state in their own words exactly what it is that they are being asked to solve. Expect them to discuss their strategies and their reasoning. Get them to explain to each other, for example, how they decided which bill was which or why November is probably not an average month (higher than average sunshine in many places). Encourage them to recognise and discuss the assumptions that they have had to make when answering questions. (The scenario has been highly simplifi ed to keep it manageable.)

Percentage is a very valuable mathematical tool. Its primary function is to enable comparisons. But

percentages are used in a number of different ways (20% more, less 20%, add 20%, 20% of, 120% of, 80% of, and so on). There are usually different ways of expressing, calculating, and writing the same percentage (for example, 20% = 0.20 = 0.2, which are the same as 2/10 = 1/5). Students should learn to express percentages as decimal numbers and use this format in any calculations that require use of a calculator.

You will probably need to do do some pre-teaching or revision of percentages before the students do this activity. Use examples that are similar in structure to those in the students’ book, but leave those in the activity for the students to tackle themselves.

The activity requires students to think about percentages in different ways:

- Activity One, question 1: Percentage as parts of 100 and as the proportional part of a whole.

- Activity Two, questions 2a and b: Percentage as a measure of relative increase: parts per 100 more.

- Activity Two, question 3: Percentage as a rate of interest: additional cost in dollars.

The activity specifies that the interest does not compound (flat rate). This is an appropriate simplification at this level.

Students who need a challenge could work out interest based on different payment schedules. For example, If Jimmy’s mum pays off $500 at the end of the year and 5% interest is added to the balance at the start of each year, what would she pay in total?

Start of year 1: $2,000 +$100 (5% interest) = $2,100

Start of year 2: $2,100 – $500 (payment) + $80 (interest) = $1,680

Start of year 3: $1,680 – $500 (payment) + $59 (interest) = $1,239

Start of year 4: $1,239 – $500 (payment) + $37 (interest) = $776

Start of year 5: $776 – $500 (payment) + $13.80 = $289.80

End of year 5: $289.80 (final payment)

So Jimmy’s mum would pay a total of $500 x 4 + $289.80 = $2,289.80

Points of Entry: Science

This activity provides another look at insulation, conservation, and alternative energy.* It relates back to other activities, such as Hypothermia. Use this as a starting point for more general discussions about ways of saving energy, for example, How does insulation help to save power? Apart from the hot water cylinder, where else in the house should insulation be installed? How do double-glazed windows work?

You could ask the students to research solar panels to fi nd out how they work and where the best place to install one might be. Information is readily available on the Internet and in brochures at major building supplies and plumbing warehouses. Some suppliers have units on display.

This could stimulate the students’ interest in eco-friendly choices and the economics of them. They could compare the costs and savings from solar panels with the savings from insulating the cylinder ($315 per year for $2,000 compared with $70 per year for $70) or the impact of other power-saving measures. Use Saving Power as a transition to the next activity, Using Electricity.

Answers

Activity One

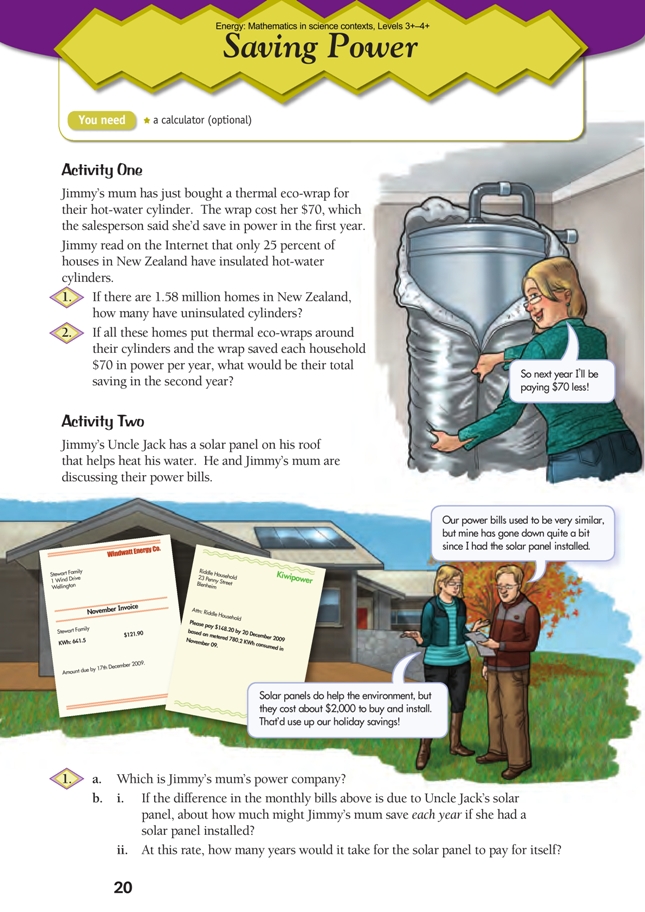

1. 1 185 000. (25% of homes have insulated cylinders so 100 – 25 = 75% must have uninsulated cylinders. 0.75 x 1 580 000 = 1 185 000)

2. $83 million. (If each home saves $70 per year, total savings amount to 70 x 1 185 000 = $82,950,000.)

Activity Two

1. a. The more expensive Kiwipower bill is for Jimmy’s home. (See Uncle Jack’s comment. But note that while Uncle Jack thinks that the difference is due to his solar panel, there could be other factors.)

b. i. Approximately $315. The difference in the monthly bills is $148.20 – $121.90, or $26.30. $26.30 x 12 months = $315.60. (This estimate assumes the difference will be the same from month

to month. In practice, winter bills are usually quite a bit more than summer bills.)

ii. Nearly 6.5 yrs. $2,000 ÷ $315.60 = 6.34

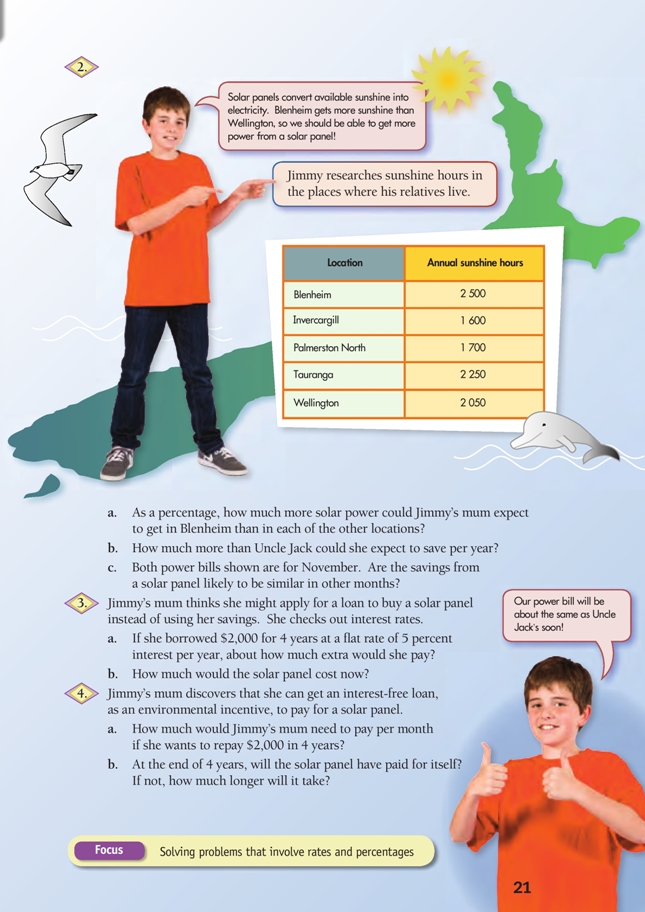

| Location | Annual sunshine hours | Blenheim’s extra hours | Extra hours as % of annual sunshine hours | Blenheim’s sunshine as % of annual sunshine hours |

| Blenheim | 2 500 | 0 | 0 | 100 |

| Invercargill | 1 600 | 900 | 56 | 156 |

| Palmerston North | 1 700 | 800 | 47 | 147 |

| Tauranga | 2 250 | 250 | 11 | 111 |

| Wellington | 2 050 | 450 | 22 | 122 |

The table represents Blenheim’s extra hours of sunshine in two ways:

Column 4: Blenheim gets 900 more sunshine hours than Invercargill. This amounts to 900 ÷ 1600 = 0.56 or 56% more.

Column 5: Blenheim gets 2 500 ÷ 1 600 = 1.56 or 156% of Invercargill’s sunshine hours.

b. Jimmy’s mum could expect to save about $385 per year, which is $69.40 more than Uncle Jack.

Blenheim gets 22% more sun than Wellington, so a solar panel in Blenheim should generate 22% more than a similar panel in Wellington. This means that, all other things being equal, Jimmy’s mum

should save 22% more than Jack. 1.22 x $315.60 = $385.

c. No. Sometimes the savings will be higher (for example, in February in a hot summer) and sometimes lower (for example, in the middle of a rainy winter).

3. a. $400. (5% of $2,000 is $100. $100 extra for 4 yrs is $400.)

b. $2,400

4. a. $41.67. (There are 48 months in 4 yrs. $2,000 ÷ 48 = $41.67)

b. No. Assuming that Jimmy’s mum saves about $385 per year, it will take another 1.2 yrs. After 4 yrs, she will have saved $1,540. $2,000 ÷ $385 = 5.2 yrs.